Insurance Carriers Are Quietly Becoming the Most Sophisticated Property Data Buyers

Jun 30, 2026

By Vin Vomero, CEO

At every appraisal conference this year, I’ve heard the same debate play out in the hallways: Should we be using AI? How much? When?

Meanwhile, three floors up at the same hotel, insurance carriers are running underwriting pilots that moved past the “should we” question a long time ago. They’re optimizing the “how well.”

The gap is striking. And it isn’t an accident.

Why Insurers Moved First

Appraisers operate under USPAP. Lenders operate under regulatory scrutiny. Both industries face compliance pressure that pushes them toward caution on AI adoption.

Insurers operate under a different pressure entirely: every bad policy is a direct P&L event. Underprice a roof, miss a vacancy signal, overlook obvious deferred maintenance on an exterior — that’s a claim you’re going to pay. There’s no committee to blame. The loss shows up on the next quarterly report.

That urgency changes everything. While other property verticals debate adoption frameworks, insurers are debating model thresholds.

What Carriers Are Actually Operationalizing

The use cases insurers are deploying today aren’t speculative pilots. They’re production workloads:

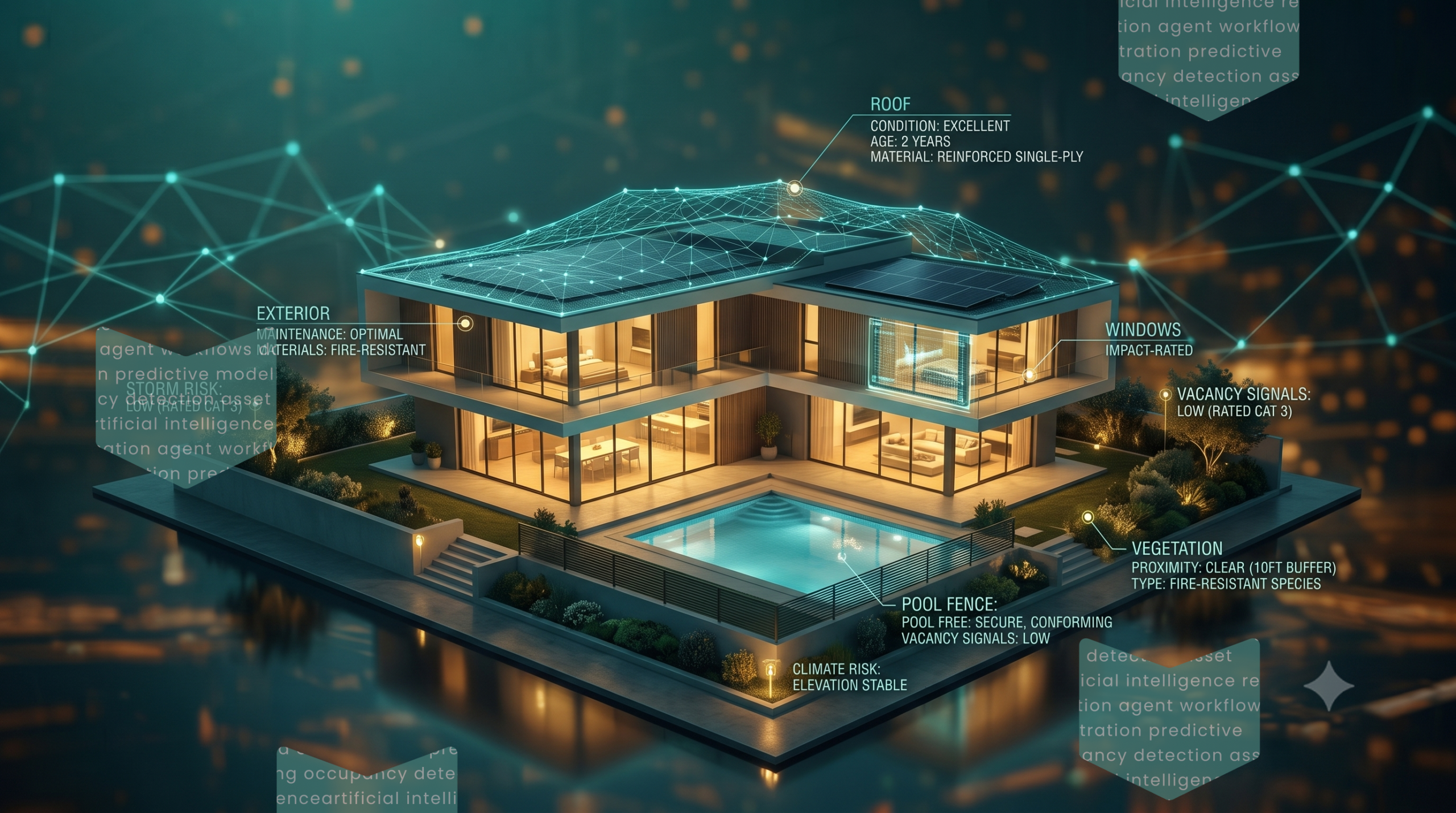

Roof Condition Scoring at Bind

Agentic solutions, computer vision and visual language models grade roof material, age signals, and visible damage from aerial and street-level imagery — before a policy is bound. Carriers are flagging high-risk roofs for inspection upfront rather than discovering them at claim time, often using signals like tarped roofs as an immediate red flag.

Exterior Damage and Hazard Detection

Overgrown vegetation, tarps, missing shingles, debris, pool fencing — all detectable from imagery, all material to risk. The same condition signals that feed AVMs and underwriting models feed actuarial models too. Increasingly, carriers are layering detailed damage detection on top of broader condition scoring to quantify risk at a granular level.

Vacancy and Occupancy Signals

Boarded windows, untended yards, lack of seasonal change across image vintages. Vacancy is one of the strongest predictors of loss, and visual intelligence surfaces it without a human ever. driving by

Claims Triage

Post-event imagery — storm, fire, flood — routed through condition models to prioritize adjuster deployment. The carriers doing this well are settling legitimate claims faster and catching fraud patterns earlier.

What Other Industries Can Learn

Three takeaways for lenders, asset managers, and PropTech operators watching this shift:

- Financial urgency beats compliance urgency. The verticals adopting fastest are the ones where bad data carries an immediate price tag. If your team is still debating AI adoption philosophically, you’re already behind the carrier underwriting the same property.

- Visual intelligence is becoming portfolio infrastructure, not a point tool. Insurers aren’t buying one model. They’re building image pipelines that serve underwriting, renewal, and claims simultaneously.

- The data is already in your systems. Carriers didn’t commission new inspections to make this work. They operationalized imagery they already had — the same imagery sitting in lender and servicer databases right now. As we’ve written before, your property photos are worth more than you think.

The Climate Variable

Here’s the forward-looking piece. As climate risk reshapes catastrophe modeling, carriers can’t price annual policies against five-year-old property snapshots. Condition drift matters. Material composition matters. Maintenance signals matter.

Visual property intelligence isn’t a competitive edge for insurers anymore. It’s becoming table stakes.

Which raises a real question for everyone else in the property ecosystem: when your insurance counterparty knows more about the asset than you do, what does that mean for your underwriting?

Curious how visual intelligence fits into your risk or underwriting workflow? Talk to our team.